Equity Release Council Members

Covered by the FSCS

Understand How Equity Release Works

Get a clear, unbiased explanation of equity release to help you make an informed decision

Authorised and regulated by the Financial Conduct Authority

The Lenders We Work With

We give Whole-of-market advice, ensuring that you get the best solution available

What people like you are saying

We pride ourselves on our ability to deliver a great service to our customers.

Download your FREE Guide.

It explains:

What is equity release?

What could equity release do for you and your family?

Is equity release the right decision for you?

Things you should consider

What are the alternatives to equity release?

What Is Equity Release & How Does It Work?

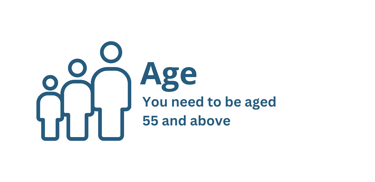

Equity release lets homeowners aged 55 or over access money tied up in their home – without having to move or make monthly repayments.

The most common type is a lifetime mortgage, where the loan and interest are repaid from the property’s value when it’s sold (usually after you pass away or move into long-term care).

Key Benefits:

Access tax-free cash, typically as a lump sum

No contractual payments - but you can make payments if you wish

Maintain ownership of your home

Spend the money how you choose including but not limited to - home improvements, helping family, or boosting retirement income

Top Six Reasons for Releasing Equity

Benefits & Considerations of Equity Release

Equity release can offer flexibility in later life, but it isn’t right for everyone.

Understanding both the potential advantages and the key considerations upfront helps you decide whether it’s something worth exploring further.

Potential Benefits

Access funds without moving home

No required monthly repayments

Important Considerations

Interest builds up over time

Reduced inheritance

Impact on benefits and entitlements

You can unlock some of the value in your property while continuing to live there, retaining security and familiarity.

Depending on the plan, funds can be taken as a lump sum or released gradually over time to suit different needs.

Most plans do not require monthly repayments, which can help manage outgoings during retirement.

If no repayments are made, interest is added to the loan, increasing the amount repaid when the plan ends.

Because the loan is repaid from your property, the value of your estate may be reduced.

Releasing funds can affect eligibility for certain means-tested benefits.

Flexible ways to release money

Frequently asked questions

Who is equity release for?

Equity release is generally designed for homeowners aged 55 or over who want to access some of the value in their property without moving.

Suitability depends on individual circumstances, which is why regulated advice is important.

What protections exist for homeowners?

Most plans include safeguards such as the right to remain in your home for life and a no-negative-equity guarantee, meaning you or your estate will never owe more than the value of your property.

How does equity release work in simple terms?

Equity release allows you to unlock money from your home while continuing to live there.

The most common option is a lifetime mortgage, where funds are released as a lump sum or in stages, under agreed terms.

Will I still own my home?

With most equity release plans, including lifetime mortgages, you retain ownership of your home and continue to live there as your main residence, provided the terms of the plan are met.

Is equity release safe?

Modern equity release products are regulated and designed with consumer protections in place.

When arranged through a regulated adviser and a lender that follows industry standards, equity release can be a secure option.

Do I need professional advice?

Yes. Equity release is a long-term financial decision, and regulated advice ensures any recommendation is suitable, clearly explained, and considers alternatives as well as potential risks.

Are you eligible?

To be eligible for Equity Release you need to at least meet the following criteria

How does the Process Work?

A Service You Can Trust

Authorised and regulated by the Financial Conduct Authority

Start Your Free, No-Pressure Consultation

Our experts are ready to help you understand how equity release works — and whether it’s right for you.

FCA-Regulated | Confidential | No Pressure

A lifetime mortgage is a loan secured against your home. To understand the features and risks, ask for a personalised illustration. Equity release will reduce the value of your estate and may affect your entitlement to means tested benefits.

Your home may be repossessed if you do not keep up contractual repayments on your mortgage.

Visit the FCA’s consumer website for more information - www.moneyhelper.org.uk

Equity release will reduce the value of your estate and may affect your entitlement to means-tested benefits

Home Equity Release is a trading style of Home Financial Services Ltd

which is an appointed representative of Cornerstone Finance Group Ltd

which is authorised and regulated by the Financial Conduct Authority.

Cornerstone Finance Group Ltd is registered in England & Wales. No. 08458702.

Registered Office: Unit E Copse Walk, Pontprennau, Cardiff, Wales, CF23 8RB.

Cornerstone Finance Group Ltd (FCA No. 767202)

Home Financial Services Ltd is registered in England and Wales No. 15250542

Registered office: Quest House, Fortran Road, St Mellons, Business Park, Cardiff, CF3 0EY.

Home Financial Services Ltd (FCA No. 1013614)

Telephone : 02922 807160

The Financial Conduct Authority does not regulate taxation and trust advice

Copyright © 2026 Home Financial Services - All Rights Reserved.