Expert Equity Release Advice:

Independent, FCA-Regulated Advice Tailored to You

Speak to an FCA-regulated, whole-of-market adviser and see how much you could release from your home: with no pressure or commitment.

✓ No Obligation Conversation

✓ Qualified and FCA Regulated

✓ Whole-of-Market Access

Access wealth tied up in your property

Fund personal goals and priorities

Avoid downsizing and stay in the home you love

Equity Release Council

Registered Members

FCA Regulated

Qualified Advisers

Whole of Market

100% Independent Advice

No Obligation

Free Initial Assessment

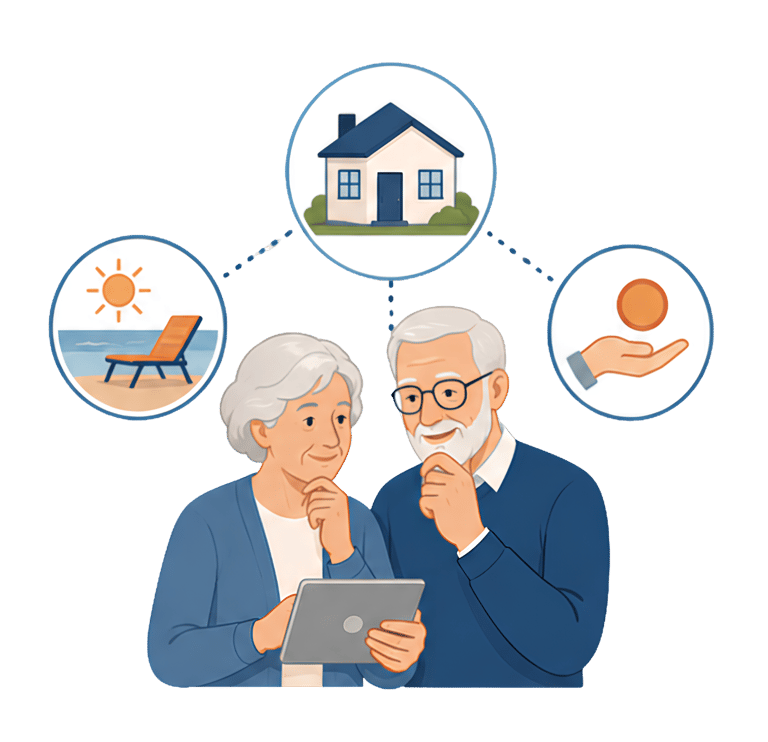

Explore Whether Equity Release Could Support Your Plans

We're here for your situation, these are the most common reasons to release equity.

Supplementing your retirement income

You might be "asset rich, cash poor" where you have a valuable home, but limited pension income. Releasing some equity tops up what comes in each month, without having to move.

Covering everyday living costs

Managing inflation and rising bills

Maintaining your standard of living

Home improvements and adaptations

You'd rather stay in your home than move, and released equity is a common way to fund the work that makes staying possible and comfortable.

Renovations, extensions, new kitchens or bathrooms

Accessibility changes e.g. stairlifts, walk-in showers

Energy-efficiency upgrades

Helping family members now

A significant share of equity release customers use the funds as a "living inheritance" - giving while they're here to see it make a difference.

Helping children onto the property ladder

Paying university costs

Assisting with debt repayment

Supporting family through major life events

Discover how releasing equity from your home could provide greater financial flexibility for retirement, home improvements, family support, or debt consolidation. Speak with our specialists to explore your options.

Is equity release right for me?

✓ No Obligation Conversation

✓ Qualified and FCA Regulated

✓ Whole-of-Market Access

Repaying existing debt or mortgages

Some homeowners reach retirement with borrowing still outstanding, and use equity release to simplify their finances and remove monthly commitments.

Paying off an interest-only mortgage at maturity

Clearing personal loans or credit card debt

Reducing monthly repayment commitments

Could Your Home Help Fund Your Next Chapter?

How much could you release?

Enter a few details about your property and age to get an instant estimate of how much tax-free cash you may be able to unlock.

Calculate my release

✓ No Obligation Conversation

✓ Qualified and FCA Regulated

✓ Whole-of-Market Access

Start Exploring Your Equity Release Options

Now that you have an indication of how much you could release, speak with one of our advisers to understand the plans available and whether equity release is right for your circumstances.

Understanding Equity Release

Unlock the Value in Your Home Without Moving

Equity release allows you to access some of this value as tax-free cash while continuing to live in the home you own and love.

Whether you're looking to supplement retirement income, fund home improvements, help family members financially, or simply create greater financial flexibility, equity release can provide access to funds without the need to sell your property.

How Does a Lifetime Mortgage Work?

A lifetime mortgage is the most popular form of equity release in the UK.

With a lifetime mortgage, you borrow against the value of your home while retaining full ownership. The loan is secured against your property and is usually repaid when the property is sold, typically after you pass away or move into long-term care.

Unlike a traditional mortgage, there are generally no required monthly repayments. Instead, interest can be added to the loan balance over time.

You May Choose To:

Take a lump sum

Access money gradually through a drawdown facility

Make optional repayments to reduce interest

Repay part of the loan without committing to regular payments

Equity release can provide access to tax-free cash while allowing you to remain in your home. Discover how modern plans are regulated and designed with important consumer protections in place.

✓ No Obligation Conversation

✓ Qualified and FCA Regulated

✓ Whole-of-Market Access

What is equity release?

For many homeowners aged 55+, a significant portion of their wealth is tied up in their property.

Key benefits

✓ Remain in your home

✓ Access tax-free cash

✓ Retain ownership of your property

✓ Flexible options for taking funds

✓ No mandatory monthly repayments on most plans

✓ FCA-regulated products with consumer protections

Your Protections

Modern equity release products include a range of safeguards designed to protect homeowners.

Equity Release Council Standards

‣ No Negative Equity Guarantee

‣ Right to remain in your home for life

‣ Option to move home

‣ Interest rate fixed for life

‣ Ability to make repayments

Explore Your Options, Protected Every Step of the Way

Our 4 Step Process

Equity release is a significant decision, so we keep the process clear and straightforward while ensuring you fully understand your options.

Initial Discussion

We start with a conversation to understand your situation, your property, and what you’re looking to achieve. We’ll answer your questions and explain how everything works, with no obligation to proceed.

Exploring Your Options

We explain how equity release works in simple terms, including how interest is applied and what it means long term. We also discuss any alternative options so you can make a fully informed decision.

Personalised Recommendation

If equity release is appropriate, we provide a recommendation tailored to your circumstances and clearly explain the costs, risks, and long-term impact.

Ongoing Support

If you decide to proceed, we manage the process through to completion and remain available to support you in the future as your circumstances change.

From your initial conversation through to completion, we'll guide you through every stage, explain your options in plain English, and ensure you have the information needed to make an informed decision.

✓ No Obligation Conversation

✓ Qualified and FCA Regulated

✓ Whole-of-Market Access

How does it work?

1

2

3

4

A Clear, Straightforward Advice Process

Frequently asked questions

Our advisers are here to provide clear answers, explain your options, and help you decide whether equity release is right for your circumstances.

✓ No Obligation Conversation

✓ Qualified and FCA Regulated

✓ Whole-of-Market Access

Still Have Questions About Equity Release?

Equity Release Council

Registered Members

FCA Regulated

Qualified Advisers

Whole of Market

100% Independent Advice

No Obligation

Free Initial Assessment

A lifetime mortgage is a loan secured against your home. To understand the features and risks, ask for a personalised illustration. Equity release will reduce the value of your estate and may affect your entitlement to means tested benefits.

Your home may be repossessed if you do not keep up contractual repayments on your mortgage.

Visit the FCA’s consumer website for more information - www.moneyhelper.org.uk

Equity release will reduce the value of your estate and may affect your entitlement to means-tested benefits

Home Equity Release is a trading style of Home Financial Services Ltd, which is an appointed representative of Cornerstone Finance Group Ltd, which is authorised and regulated by the Financial Conduct Authority. Cornerstone Finance Group Ltd is registered in England & Wales. No. 08458702. Registered Office: Unit E Copse Walk, Pontprennau, Cardiff, Wales, CF23 8RB. Cornerstone Finance Group Ltd (FCA No. 767202) Home Financial Services Ltd is registered in England and Wales No. 15250542 Registered office: 4 Castleton Court, Fortran Road, St Mellons, Cardiff, CF3 0LT. Home Financial Services Ltd (FCA No. 1013614) Telephone: 02922 807160 Email: enquiries@home-equityrelease.co.uk.

We are a credit broker, not a lender. We are whole of market broker. We may receive commission from the lender and this amount varies between lenders.

© 2026 Home Financial Services - All Rights Reserved.